GoldenEye

Well-Known Member

- Thread starter

- #1

I've seen a lot of threads about people saying they've had terrible luck with car dealerships and their car purchasing experiences. This may be a bit of a read but I think I can help future car purchases go a little smoother for some of you. The following is based on my 20 plus years experience in the car business and WA State laws rules and regulations. There is a lot more than listed below but this should be generalized enough to assist some future purchases.

A couple of simple tips:

*Don't be rude, condescending or generally unpleasant. You catch more flies.....well you know how it goes...

*Don't lie, tell the truth and it will save you from looking stupid when the truth comes out...

*If you don't like the salesman, ask for another one, super simple...

*If you come across a dirtbag dealership, leave right away...

If you're searching for a vehicle:

*First of all you need to know if the vehicle exists, yep, car dealerships do advertise vehicles that aren't even built yet OR have been sold already (online).

*Searching for a dealership that might have one? read some reviews before you go buy it or place a deposit.

*Deposits, understand what their definition of a deposit is before you place it, get it in writing. ETAs are VERY subjective, don't be surprised if it takes longer or shorter than promised.

*You go to a dealership because you know they have a car you want (or maybe you're just looking) make sure you have a good salesman. How can you tell? It's not hard, if the salesman comes out and jokes around a bit, asks some questions about you that aren't really car related and is generally pleasant to be around, he's building rapport and there's a good chance you'll have a good experience with that salesman. If a salesman comes out and goes straight for the meat and potatoes he's likely a bottom sucker or a shitty salesman in general who's desperate for a commission.

You go into a dealership because you called them about an advertised vehicle and they have it, here are some things that are important to know:

*The dealership might require certain packages on their vehicles: For example; LoJack, window tint, ceramic coating, PPF, mud flaps etc...accessories that you might not really want. You can try to negotiate these out but sometimes it's going to be hard because it's either already installed or already planned to be installed. In this case, you either live with it or go somewhere else.

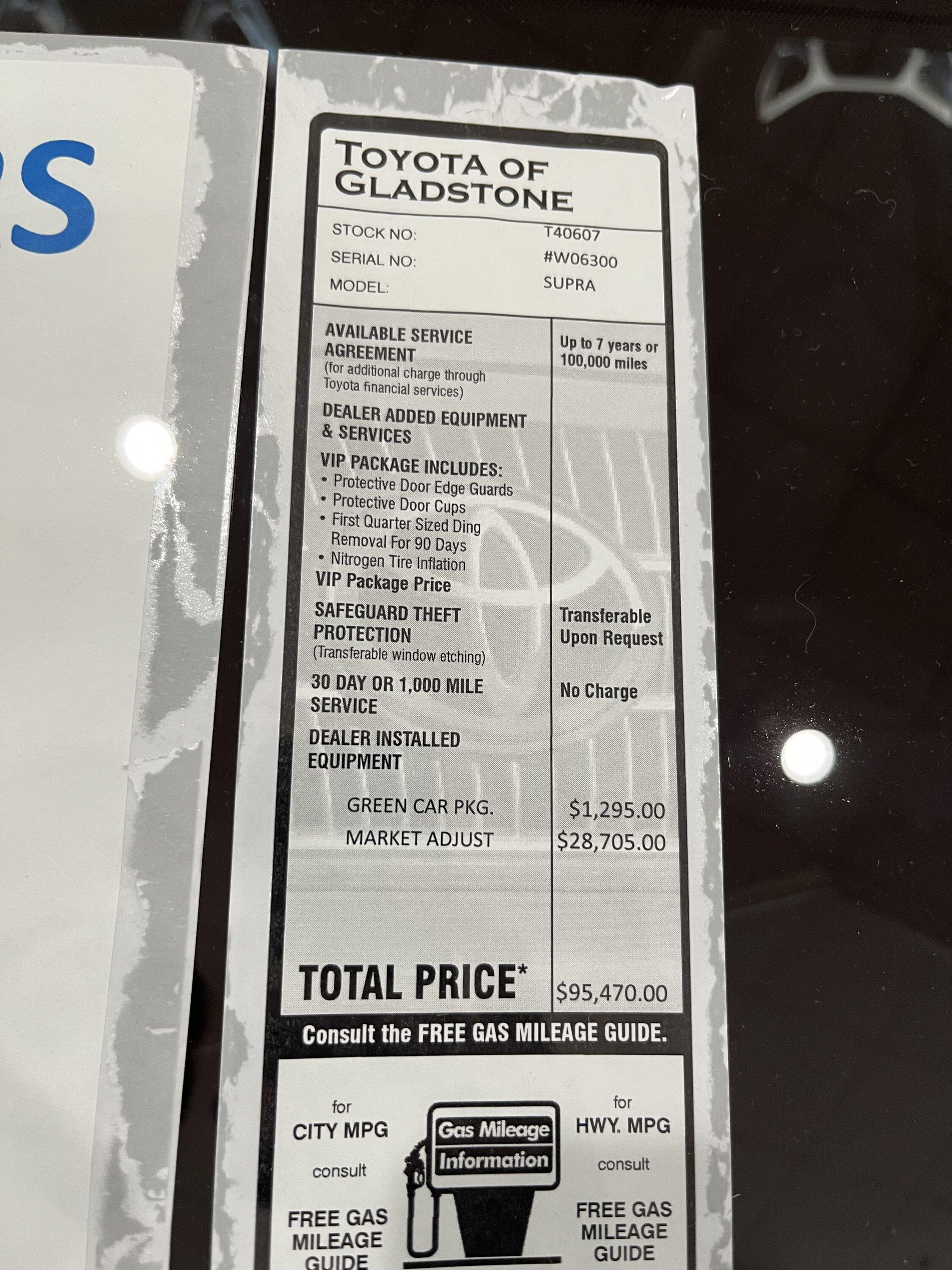

*If a car dealership says that a car was ordered by another client then they backed out and they ordered it with a certain package like all weather floor mats or tint or a fancy wax etc...easy way to tell if that's true or not is: it will be on the monroney sticker under accessories and if it is, it's definitely not coming off, or price negotiated.

Price of the car:

*Be reasonable, I know everyone wants a good deal but don't lead off with $5k off the sticker price unless you know for sure it's overpriced.

*Don't ever pay a second stick that says something like adjusted market value or "because we can" type of markup. ONLY pay a second sticker if you get something for it, again, like tint, all weather floor mats etc...AND you agree to it.

*If it's a new car you can ask to see the invoice, they might show you, but that doesn't mean they'll sell it to you for that price.

*The car dealership doesn't want you to pay cash, so don't try and use that as a tool of negotiation. They make money off of interest rates from the banks.

*Tax & License fees, don't finance them if you can help it. Whatever the tax and license fees are, try to put that as a downpayment. Common misconception is your car loses a bunch of value as soon as you drive off the lot and you're upside down in your loan. Well, some cars do lose value quick, however a lot of times it's financing the tax and license fees that put you upside down.

Trade in:

*It doesn't matter what you say you want for the car, the dealership only has one number they think it's worth, they just might not give you all of it...

*Example of a trade: let's says it's paid for, Honda Civic and it's ACV (actual cash value) is $4k, the salesman will come back and tell you it's worth $2k, this way they make an extra $2k on your deal. You'll know they're holding back because they'll come back after negotiations with, let's say $3k. That extra $1k didn't just come from thin air, know what you're car is worth, realistically...

Finance:

*If you tell the salesman your credit score is 750 on "Credit Karma" you deserve to get smacked, seriously...

*Do you finance through your own bank or do you let the dealership find financing for you? This all depends on the state laws I guess, here in WA car dealerships are not legally allowed to mark up interest rates from "Credit Unions" but they can hold points with banks. Fun fact: if you let a car dealership pull your credit and get you financing, they're likely to get you a better deal that you could get with your own bank. How? Because they finance hundreds of car deals a month and get promotions from banks, whereas you might buy, let's say 50 (being generous) cars in your lifetime? Here in WA we have CUDL "Credit Union Direct Lending" that means the car dealership is partnered up with all major credit unions in the state and will get you the absolute best interest rate your credit approves you for. If you are a member of a credit union and they tell you to come in and do financing through them instead, that's a breach of THEIR contract, yep, that's right, the credit unions are the ones who invented CUDL...

*Warranties, you aren't required to buy them, if you don't want it, say no, period.

*Gap, buy it every time you finance a car unless you put half down payment of the car's value.

Promised items:

*Salesman throws in window tint to close the deal and you shake on it. Get it in writing, it's called a "we owe" and you can obtain your copy from the salesman or finance dept. but make sure it is what it's supposed to be before you sign.

A couple of simple tips:

*Don't be rude, condescending or generally unpleasant. You catch more flies.....well you know how it goes...

*Don't lie, tell the truth and it will save you from looking stupid when the truth comes out...

*If you don't like the salesman, ask for another one, super simple...

*If you come across a dirtbag dealership, leave right away...

If you're searching for a vehicle:

*First of all you need to know if the vehicle exists, yep, car dealerships do advertise vehicles that aren't even built yet OR have been sold already (online).

*Searching for a dealership that might have one? read some reviews before you go buy it or place a deposit.

*Deposits, understand what their definition of a deposit is before you place it, get it in writing. ETAs are VERY subjective, don't be surprised if it takes longer or shorter than promised.

*You go to a dealership because you know they have a car you want (or maybe you're just looking) make sure you have a good salesman. How can you tell? It's not hard, if the salesman comes out and jokes around a bit, asks some questions about you that aren't really car related and is generally pleasant to be around, he's building rapport and there's a good chance you'll have a good experience with that salesman. If a salesman comes out and goes straight for the meat and potatoes he's likely a bottom sucker or a shitty salesman in general who's desperate for a commission.

You go into a dealership because you called them about an advertised vehicle and they have it, here are some things that are important to know:

*The dealership might require certain packages on their vehicles: For example; LoJack, window tint, ceramic coating, PPF, mud flaps etc...accessories that you might not really want. You can try to negotiate these out but sometimes it's going to be hard because it's either already installed or already planned to be installed. In this case, you either live with it or go somewhere else.

*If a car dealership says that a car was ordered by another client then they backed out and they ordered it with a certain package like all weather floor mats or tint or a fancy wax etc...easy way to tell if that's true or not is: it will be on the monroney sticker under accessories and if it is, it's definitely not coming off, or price negotiated.

Price of the car:

*Be reasonable, I know everyone wants a good deal but don't lead off with $5k off the sticker price unless you know for sure it's overpriced.

*Don't ever pay a second stick that says something like adjusted market value or "because we can" type of markup. ONLY pay a second sticker if you get something for it, again, like tint, all weather floor mats etc...AND you agree to it.

*If it's a new car you can ask to see the invoice, they might show you, but that doesn't mean they'll sell it to you for that price.

*The car dealership doesn't want you to pay cash, so don't try and use that as a tool of negotiation. They make money off of interest rates from the banks.

*Tax & License fees, don't finance them if you can help it. Whatever the tax and license fees are, try to put that as a downpayment. Common misconception is your car loses a bunch of value as soon as you drive off the lot and you're upside down in your loan. Well, some cars do lose value quick, however a lot of times it's financing the tax and license fees that put you upside down.

Trade in:

*It doesn't matter what you say you want for the car, the dealership only has one number they think it's worth, they just might not give you all of it...

*Example of a trade: let's says it's paid for, Honda Civic and it's ACV (actual cash value) is $4k, the salesman will come back and tell you it's worth $2k, this way they make an extra $2k on your deal. You'll know they're holding back because they'll come back after negotiations with, let's say $3k. That extra $1k didn't just come from thin air, know what you're car is worth, realistically...

Finance:

*If you tell the salesman your credit score is 750 on "Credit Karma" you deserve to get smacked, seriously...

*Do you finance through your own bank or do you let the dealership find financing for you? This all depends on the state laws I guess, here in WA car dealerships are not legally allowed to mark up interest rates from "Credit Unions" but they can hold points with banks. Fun fact: if you let a car dealership pull your credit and get you financing, they're likely to get you a better deal that you could get with your own bank. How? Because they finance hundreds of car deals a month and get promotions from banks, whereas you might buy, let's say 50 (being generous) cars in your lifetime? Here in WA we have CUDL "Credit Union Direct Lending" that means the car dealership is partnered up with all major credit unions in the state and will get you the absolute best interest rate your credit approves you for. If you are a member of a credit union and they tell you to come in and do financing through them instead, that's a breach of THEIR contract, yep, that's right, the credit unions are the ones who invented CUDL...

*Warranties, you aren't required to buy them, if you don't want it, say no, period.

*Gap, buy it every time you finance a car unless you put half down payment of the car's value.

Promised items:

*Salesman throws in window tint to close the deal and you shake on it. Get it in writing, it's called a "we owe" and you can obtain your copy from the salesman or finance dept. but make sure it is what it's supposed to be before you sign.

Sponsored