PowerGetter

Well-Known Member

- First Name

- Randall

- Joined

- Feb 26, 2024

- Threads

- 14

- Messages

- 275

- Reaction score

- 566

- Location

- Long Beach, California

- Car(s)

- 24' Supra 3.0 MT... the Orange one

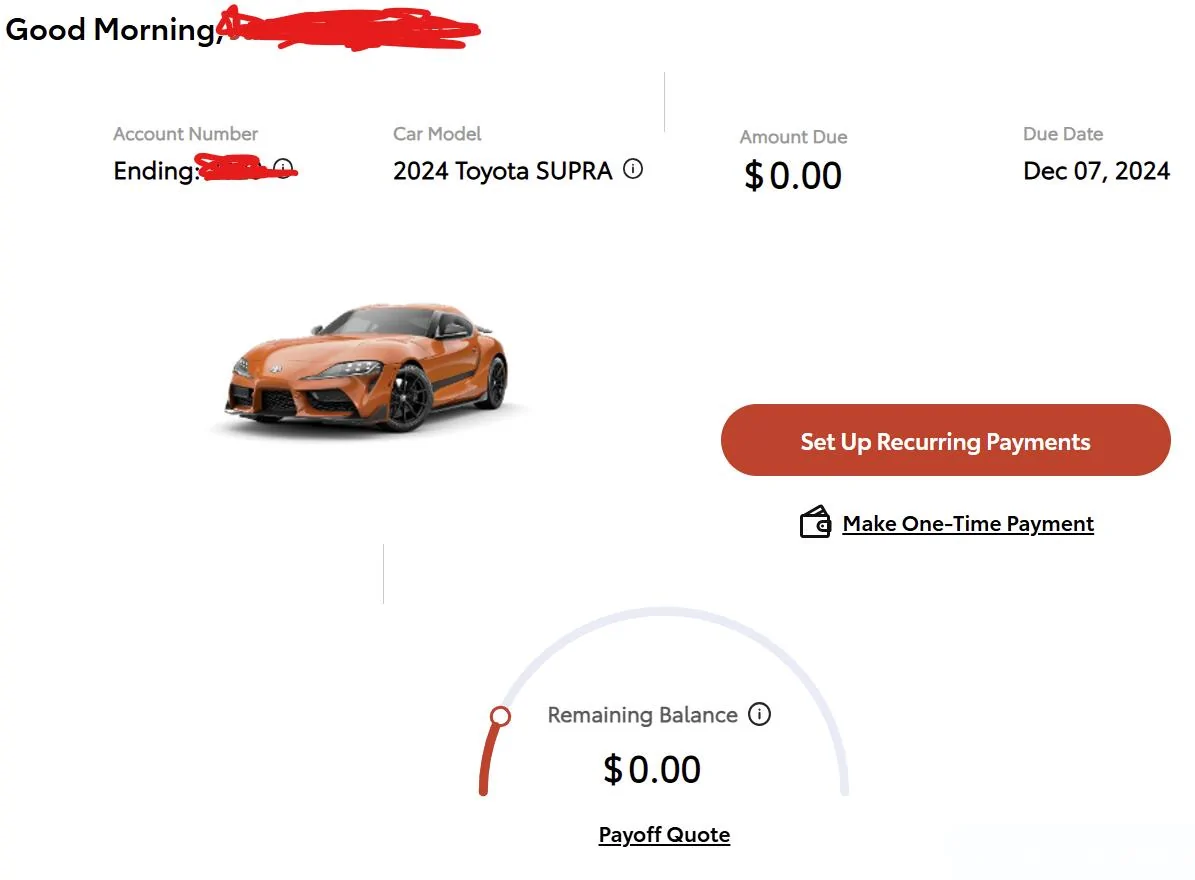

I usually leave a years worth of cash in a high yield savings, so I used a portion of that to pay the car off. Didn't touch investments or retirementIf you pulled money from a regular checking or very low yield savings account then good choice. If you liquidated an investment, even if earning less than the rate you were paying on the Supra, then it was likely not the best choice. Interest on a car loan is applied to a decreasing balance while investment yields are on increasing balances (generally). In most cases you end up earning more in your investment accounts than you pay in interest over the course of a car loan. I used to do F&I and could literally show people the math of how at the end of a 5 year car loan at say 7% the customer would have more net money if they kept their 5% 5 year CD instead of cashing it in and paying cash for their car. Probably 80% of customers couldn’t grasp the concept and cashed in the CD/other investments to pay cash, some actually accused me of lying, and only a small handful were like damn, you’re right, thanks for showing me this. Of course, this assumes you can afford the payment from current income but if you can’t you likely aren’t getting approved for a loan anyway.

") I have good credit, but the addition of the car added to my debt/income ratio so my interest on the car wasn't favorable at all. I obviously need to build the savings back up to a comfortable cushion again, but that's ok. Good advice all around though!

I have good credit, but the addition of the car added to my debt/income ratio so my interest on the car wasn't favorable at all. I obviously need to build the savings back up to a comfortable cushion again, but that's ok. Good advice all around though!